What are the trends of the hyper—casual games market worth paying attention to at the moment, – said Sergey Martinkevich, Publishing Lead at Azur Games.

The column is based on Sergey’s speech at the joint meetup of Azur Games and Google Ads, which took place in early spring and was dedicated to the development and monetization of hyper-casual games.

Sergey Martinkevich

After covid, everyone expected the stagnation of the mobile games market, but what we see now cannot be called just stagnation. eCPM is declining, profit is declining — this is a market downturn.

Let’s try to delve deeper and see what is happening in the hyper-casual niche, let’s try to understand which subgenres developers should choose today in order to increase their chances of success this year.

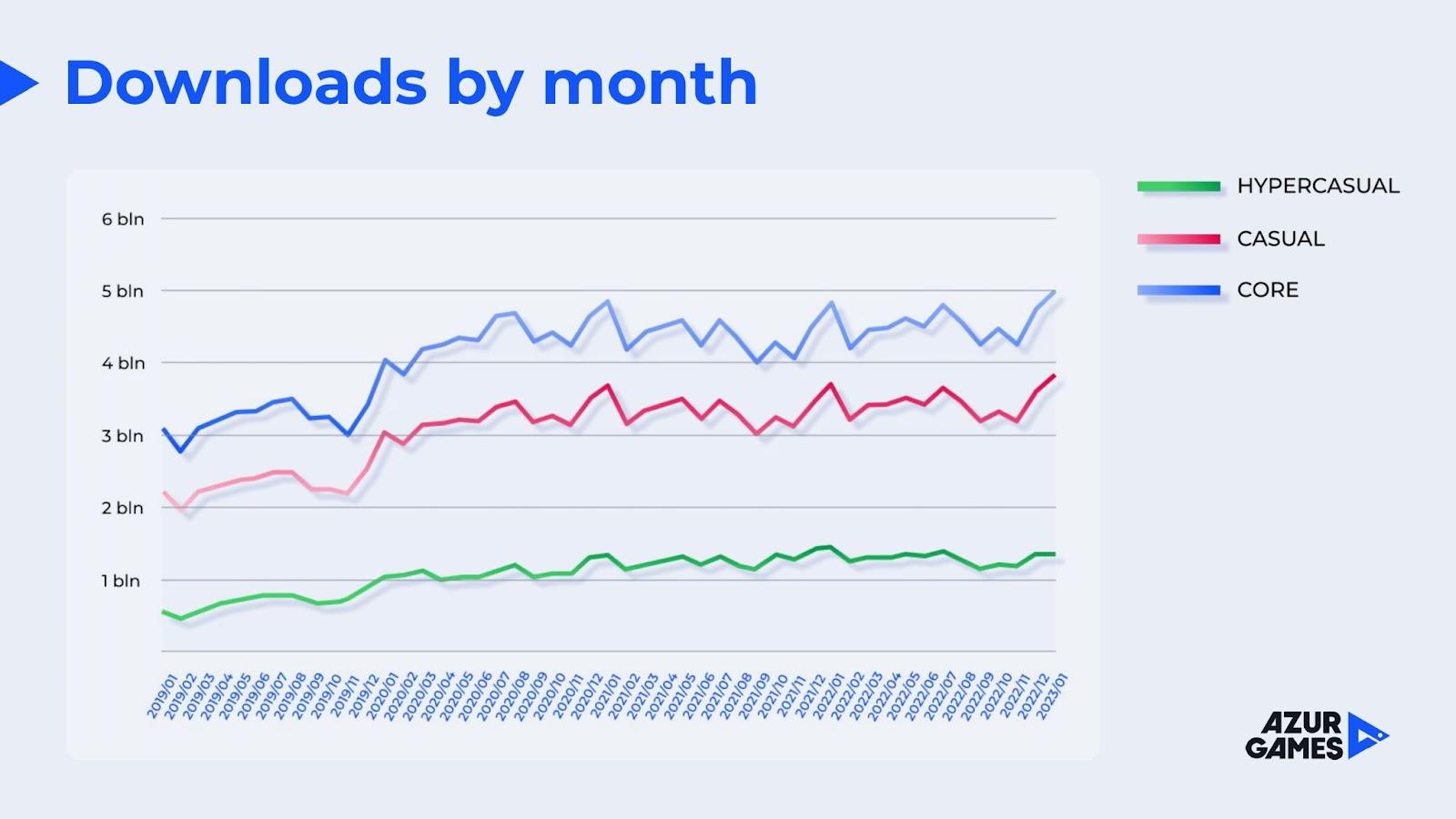

Let’s start with the volume of market downloads.

This graph shows the dynamics of downloads of casual, core and hyper—casual games per month (by core we mean both midcore and hardcore directions at once).

As we can see, the volume of downloads for both casual and core projects is growing.

As for the niche of hyper-casual games, which until recently was considered almost the fastest growing, the dynamics of its cumulative downloads does not even show significant spikes.

Some even say that the hyper-casual is dead. I won’t be so pessimistic, it’s a little more complicated.

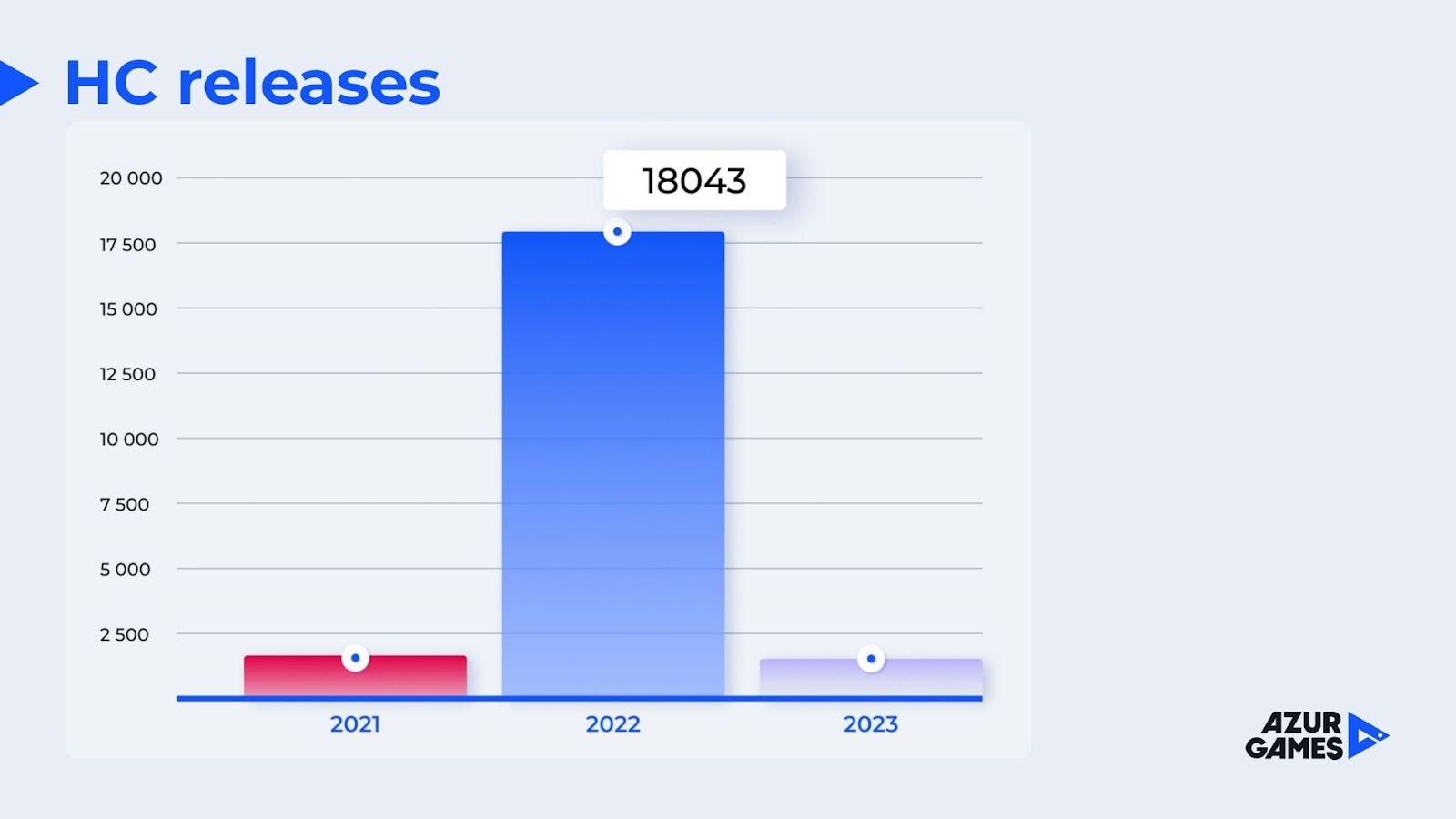

Let’s move on to the competition in the niche.

This graph shows the number of hypercausal releases by year (in total, both prototypes and commercial releases).

In 2022, compared to 2021, the number of prototypes increased 10 times. In 2023, only in January, the same number of prototypes were produced as in the whole of 2021. It is increasingly difficult for projects to stand out, there are a lot of offers in the niche.

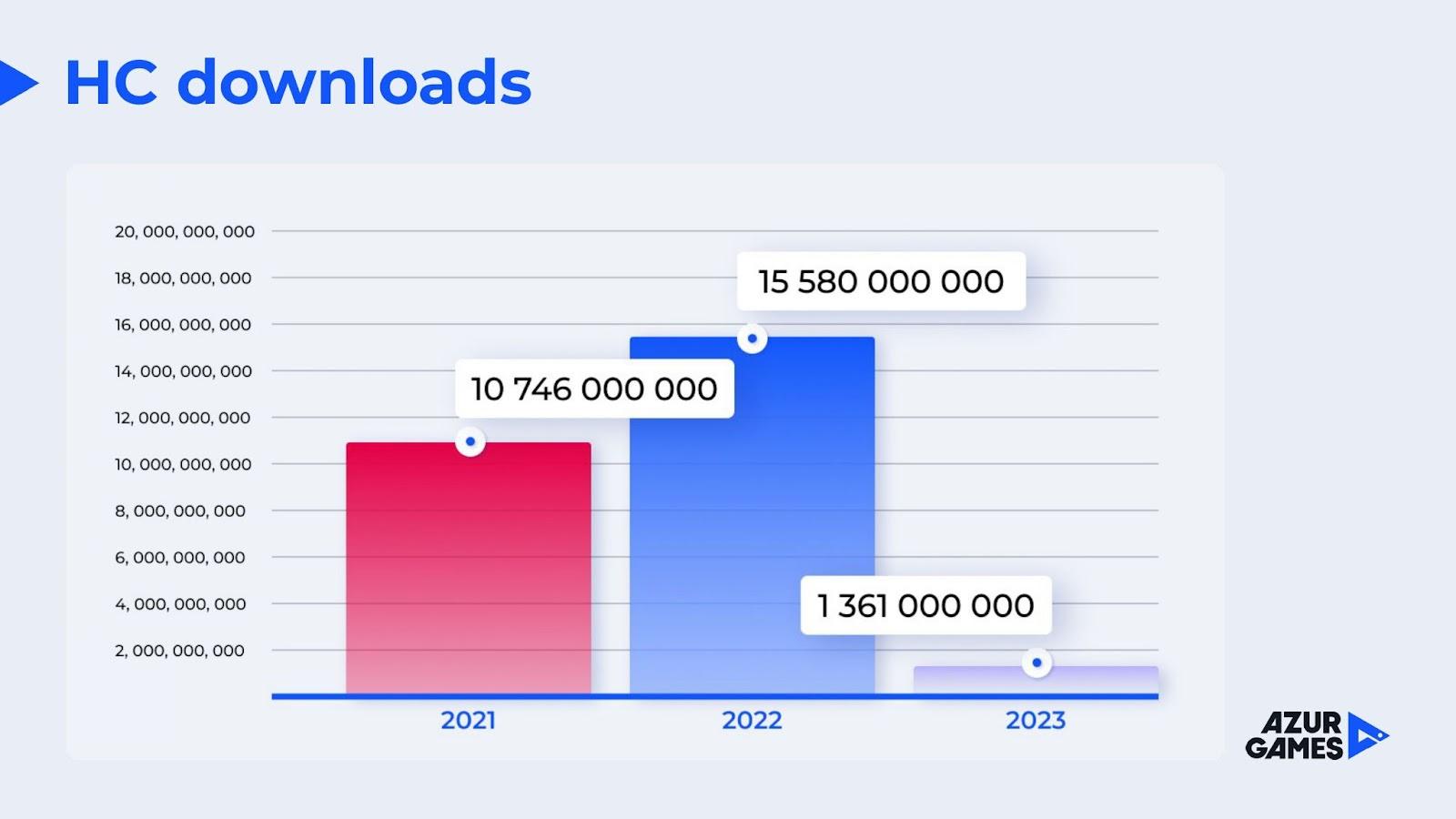

Now let’s go further and look at the volume of cumulative downloads of hyper-casual games.

In 2022, the number of downloads of hyper-casual games increased by 50% compared to 2021. Significant growth, which still does not keep pace with the growth in the number of offers.

As for the current year (as of the beginning of February), it seems to me that the final number of installations will be at the level of 2021.

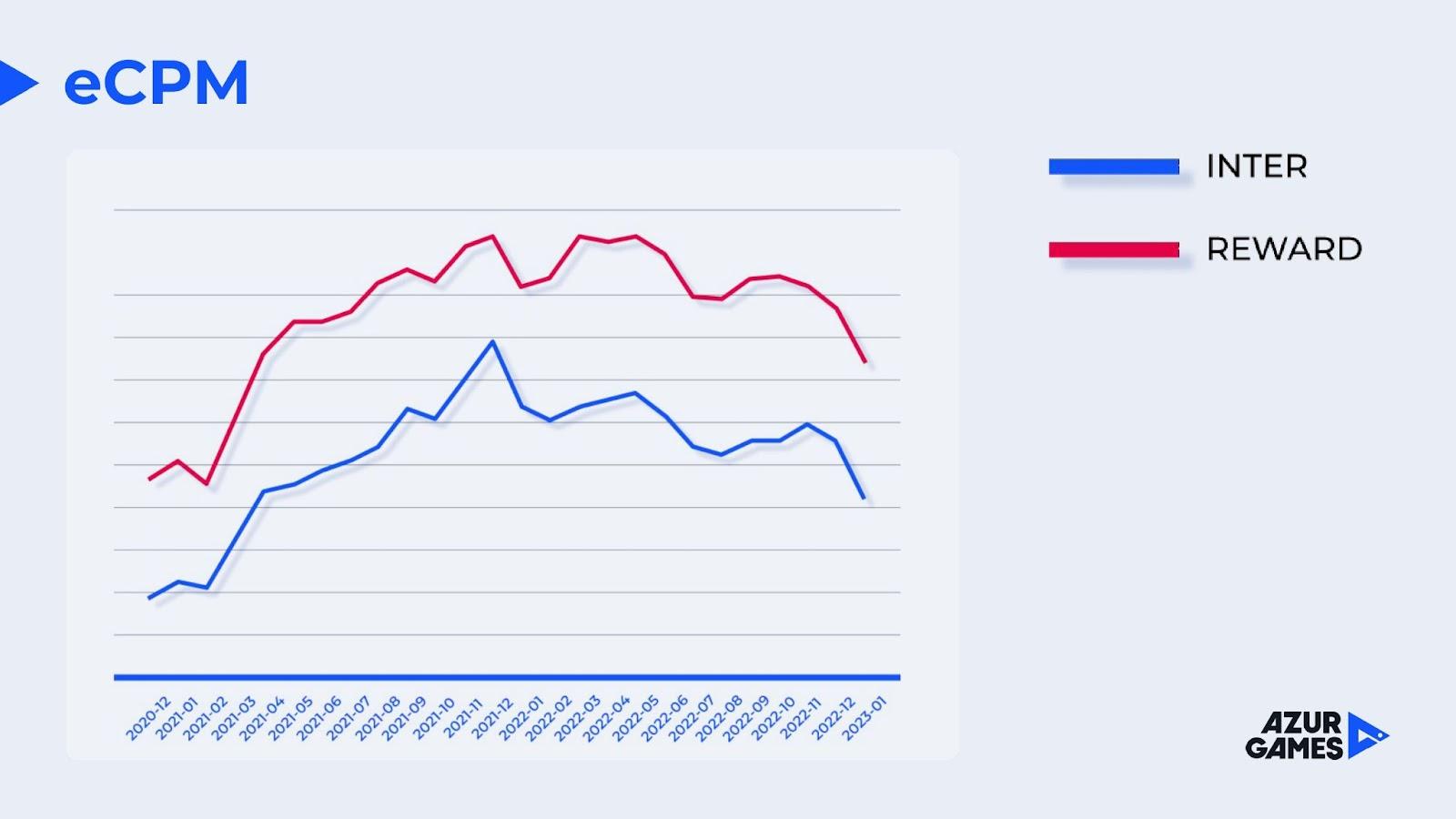

Let’s move on to monetization.

eCPM is considered one of the indicators of the “health” of the hyper-casual niche, since most of the revenue of such games comes from advertising.

We see that the peak values in the niche were during the pandemic. Then adjustments occurred. Now the fall has begun.

Not so long ago, I discussed with a producer from my team one idler — we got 300% ROAS. And I remembered that we had a very similar idler in terms of the number of reviews viewed last spring. We decided to see how comparable the eCPM projects are. The new idler had it twice as low. And yet we were able to get a good ROAS, but thanks to better onboarding, better content delivery, possibly better monetization and a low CPI.

It is possible that eCPM will still show growth within the niche, but it will no longer achieve the previous record figures.

Why is this happening? First of all, user behavior. They don’t play as much as they did during the pandemic. Large advertisers then reduce their costs. So everything is within the framework of market laws: high supply and low demand.

Let’s continue the topic of competition.

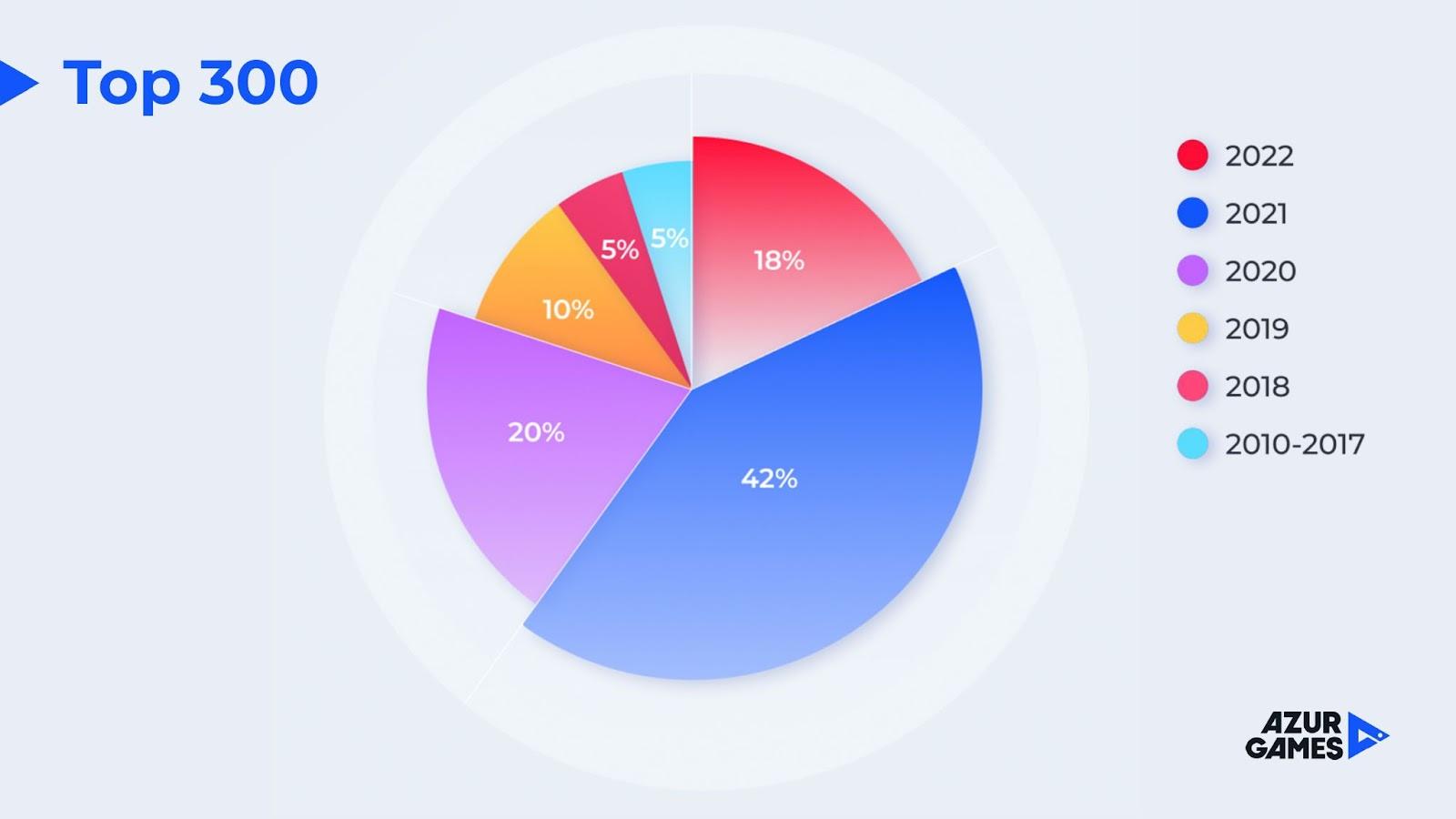

This is the top 300 games by the number of downloads at the time of writing. The schedule is divided into the years when each game from the top was released. As you can see, 2022 gave us only 18% of the games from the top. And I want to remind you that it was in 2022 that there was the highest competition. As for the non-competitive 2021, he gave 42% of the games from the top. It’s been a really productive year. As for the games released in 2020, they now account for a fifth of the top.

The good old hits are in no hurry to leave the top 300. Fruit Ninja has been there at all since 2010. Azur Games also has several similar games, for example, Stack Ball and Worms Zone.

So, what we have. The competition is crazy. The market volume is not growing. eCPM is falling. And golden hits are in no hurry to give way to new games. But not everything is so bad.

The year 2022 has given us several significant releases.

I would especially like to highlight Tall Man Run from Supersonic, which already has more than 100 million downloads by now. Why is it worth paying attention to? Because it’s a fresh runner. Appreciate the irony of the situation: it is believed that runners in the niche of hyper-casual games are no longer in trend (their downloads are falling, they are going out of fashion), and then one of the most high-profile releases of the year becomes a runner.

Fill the Fridge by Rollic Games was also released in a niche that had lost relevance at the time of the game’s release. This means that if you make a really good game, then it can take off even on a falling trend.

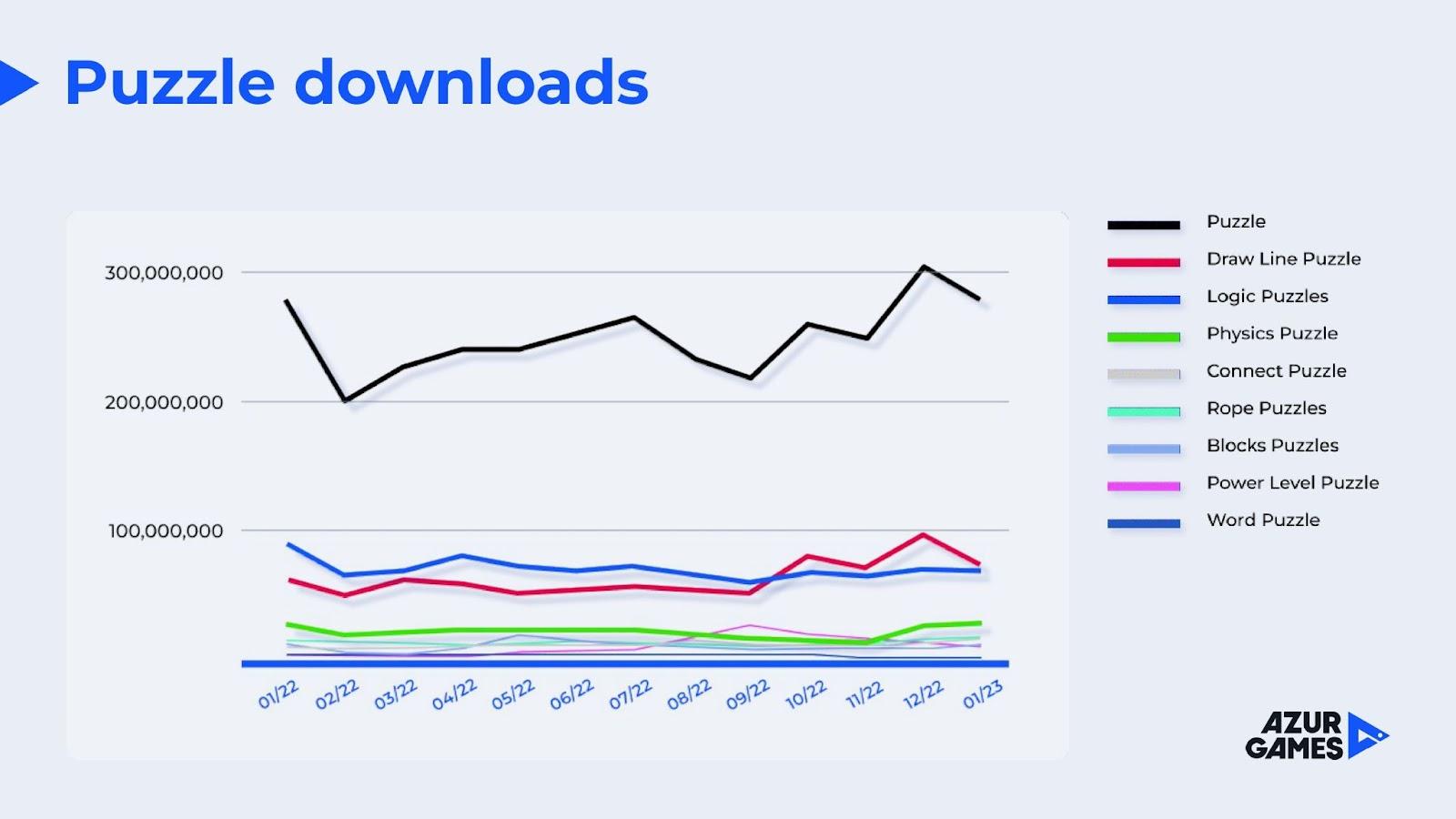

The third release worth a lot of attention last year is Save the Doge by Wonder Group. It is probably one of the reasons for the surge in downloads of the puzzle subgenre in 2022, which we will see in the charts below.

In the meantime, we are sharing the top 15 most downloaded hyper casual games of last year.

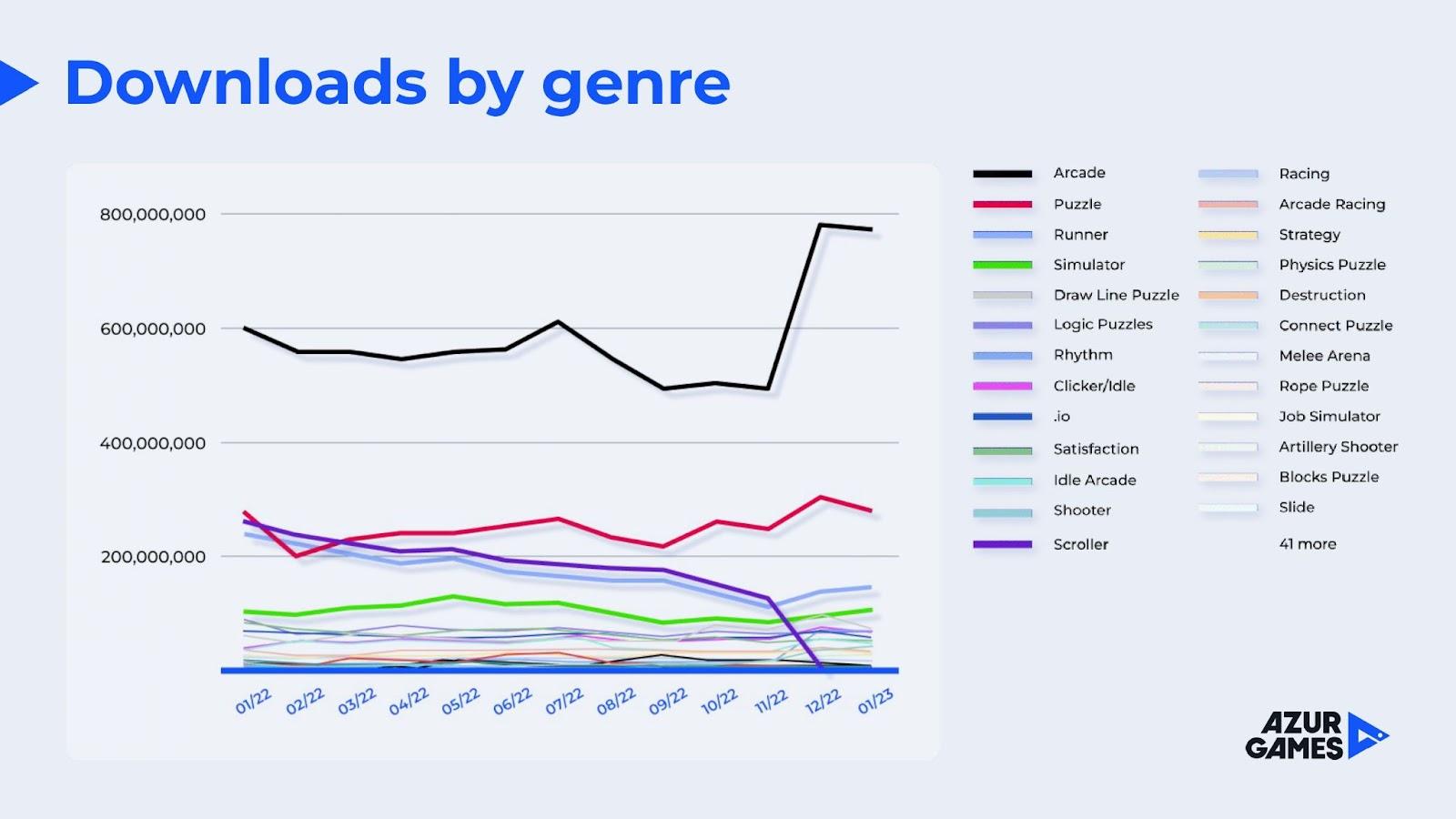

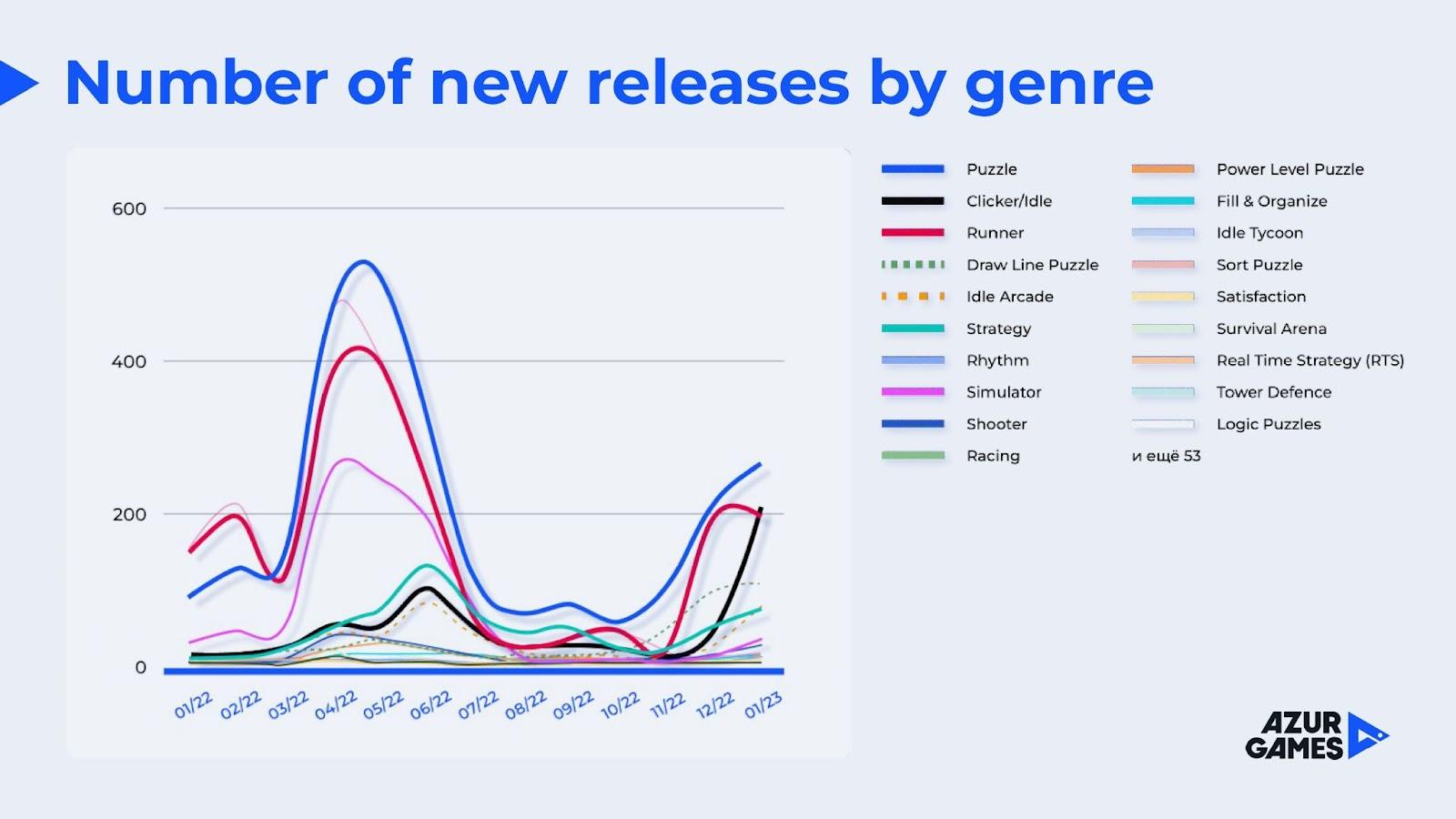

Now let’s talk about the subgenres of the hypercausal niche.

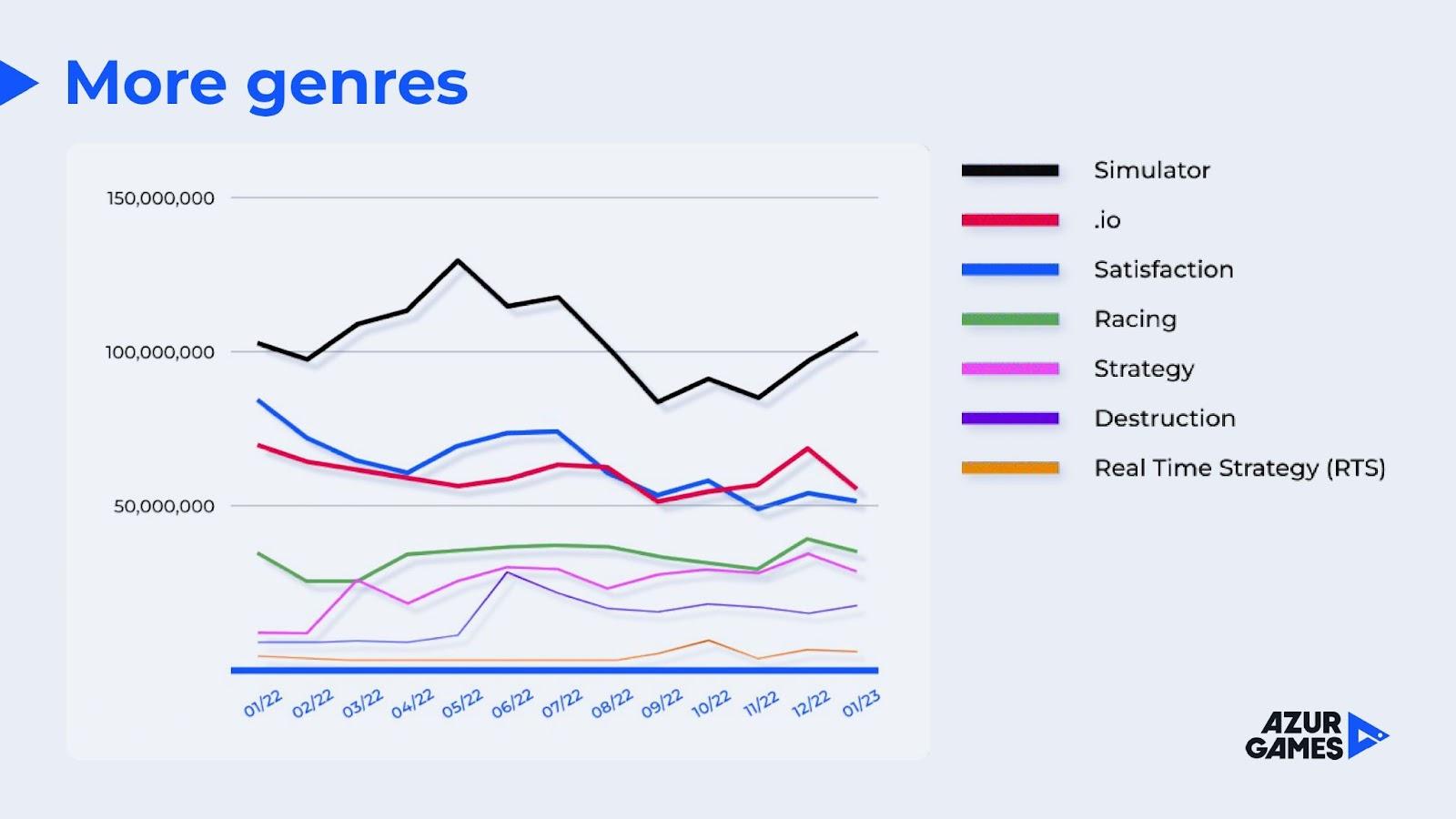

We cannot analyze arcades as an independent subgenre, since such a tag is actively assigned to a variety of games, but its popularity can be an indicator of the health of a hyper-casual niche.

Also, as for the falling purple scroller line, there is already a problem of definitions, since many analytical tools label subgenres differently and for some reason at the end of 2022 the scroller turned into a runner. In fact, it’s almost the same thing. You can notice that as soon as the scroller fell, and the runner rose a little.

We also see that puzzles and simulators show themselves quite well. It’s funny because two years ago they were considered dying subgenres in the niche.

Again, the black line is more related to the general trend, because puzzles can also overlap with other small subgenres.

But more importantly, how small subgenres develop. For example, power level puzzle did not receive any installations until mid-summer. Then, in the wake of the popularity of Save the Doge, the subgenre began to grow, and today, in general, they feel pretty good.

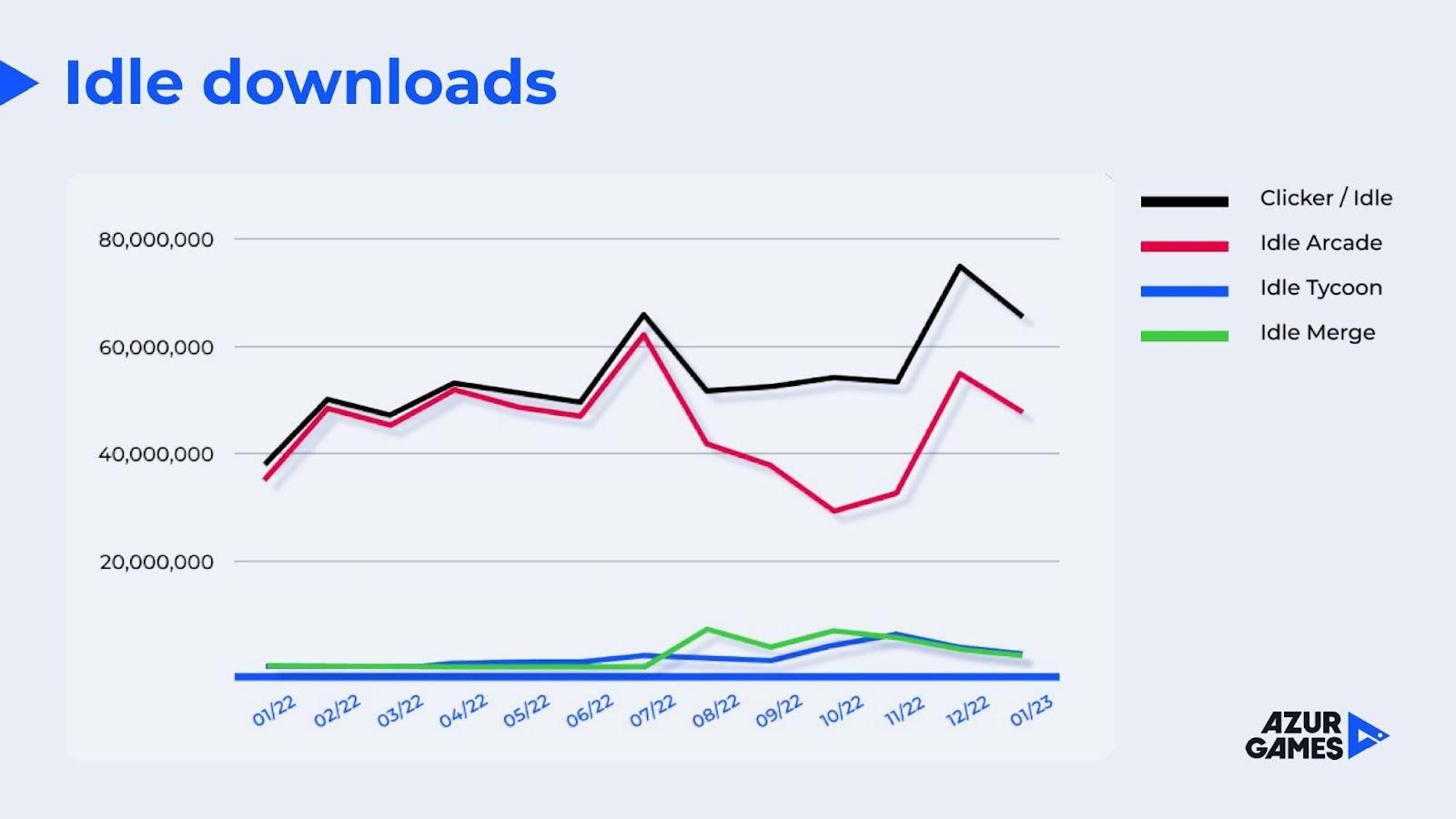

Now let’s talk about idlers.

Even if compared with the beginning of 2022, their installations have grown. And over the past two years, the growth has generally amounted to more than 100% — both in terms of installations and monetization.

Another interesting feature is the decrease in idle arcade indicators in almost all analytical tools. But this does not mean a decrease in the actual settings of the subgenre, but that its dynamics began to be measured by a group of other tags.

In general, idler downloads are growing despite the high competition.

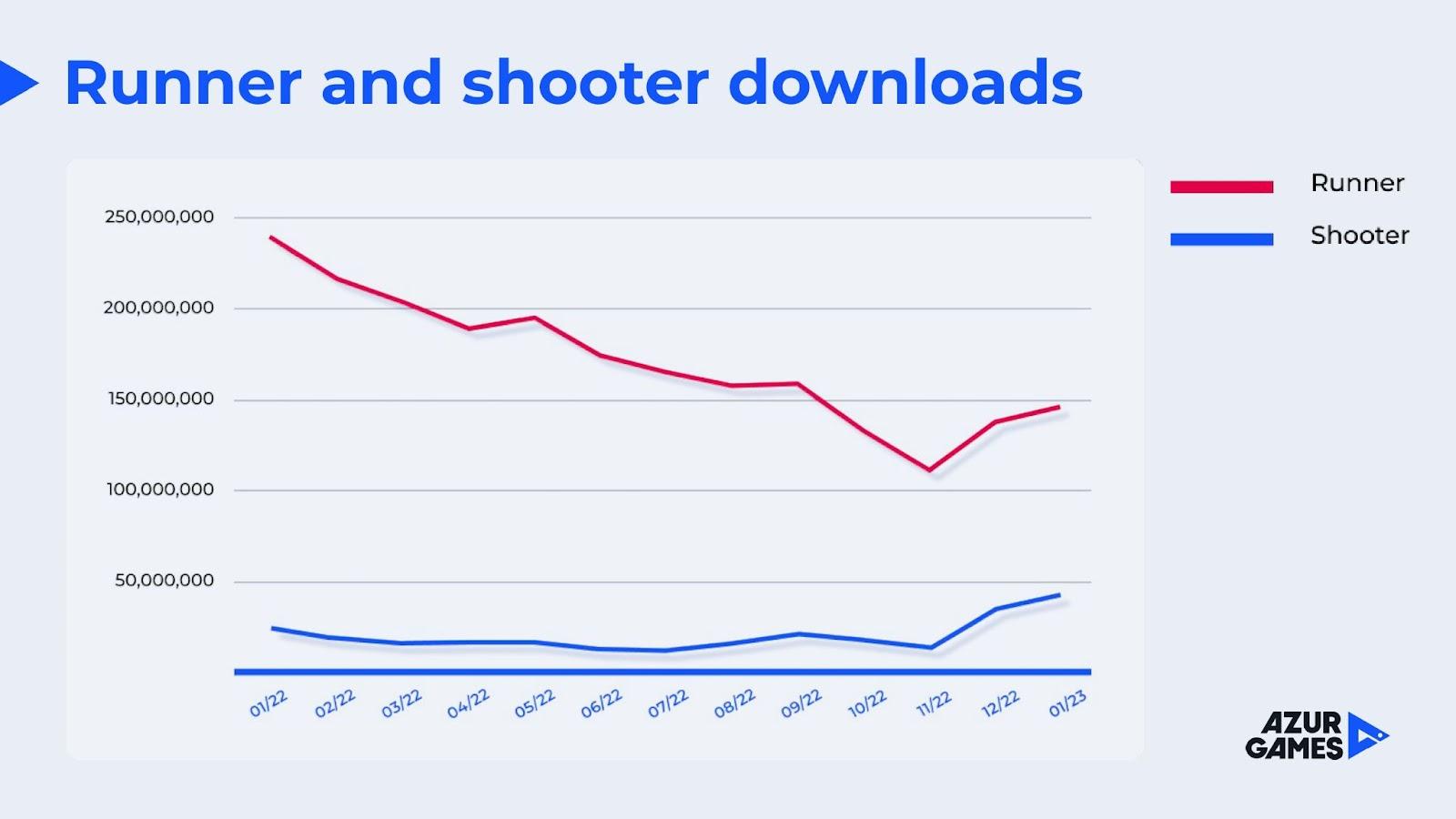

Let’s take a look at the runners and shooters.

The runner installations are still decent, and there are a lot of them in the top 300, this subgenre is very mature. But the trend is going down, despite the crazy 100 million downloads of Tall Man Run in 2022. In addition, runners are becoming increasingly difficult to scale.

Hyper-casual shooters are growing, but you have to be careful, because they are extremely difficult to scale, provide a good flow of content and game design. And here again there is a problem with tags, because hyper-casual shooters for all analytical tools are not shooters in the classical sense (from the first person). We have a Tank Stars game with over 300 million downloads, it’s a 2D game, but it’s also considered a shooter.

Satisfaction and .io are down a bit, but still have a decent number of installations. If you work in these subgenres, success here depends more on the quality of the product.

Interestingly, the number of strategy installations has tripled since the beginning of last year. And this is a fairly stable volume. So it is quite possible for developers to take a closer look at this genre.

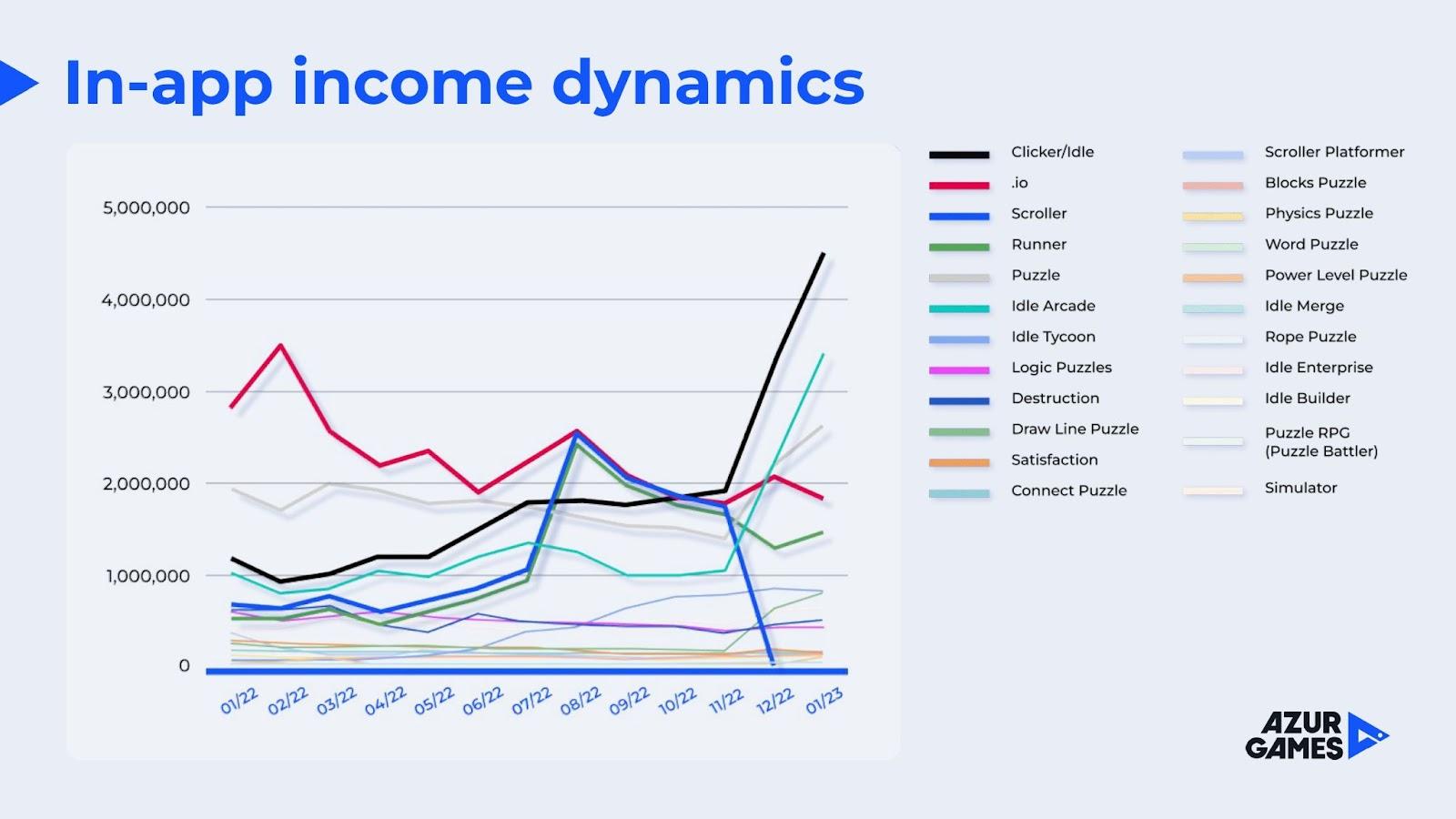

Next is a graph with IAP-monetization of hyper-casual games. The most interesting question for developers.

Clickers and idlers show amazing growth. Puzzles can also be attributed to the leaders in monetization through payments. IAP-revenue of the .io subgenre is declining, but still remains at a decent level. Runners also feel pretty stable.

Now let’s look at the information from open sources.

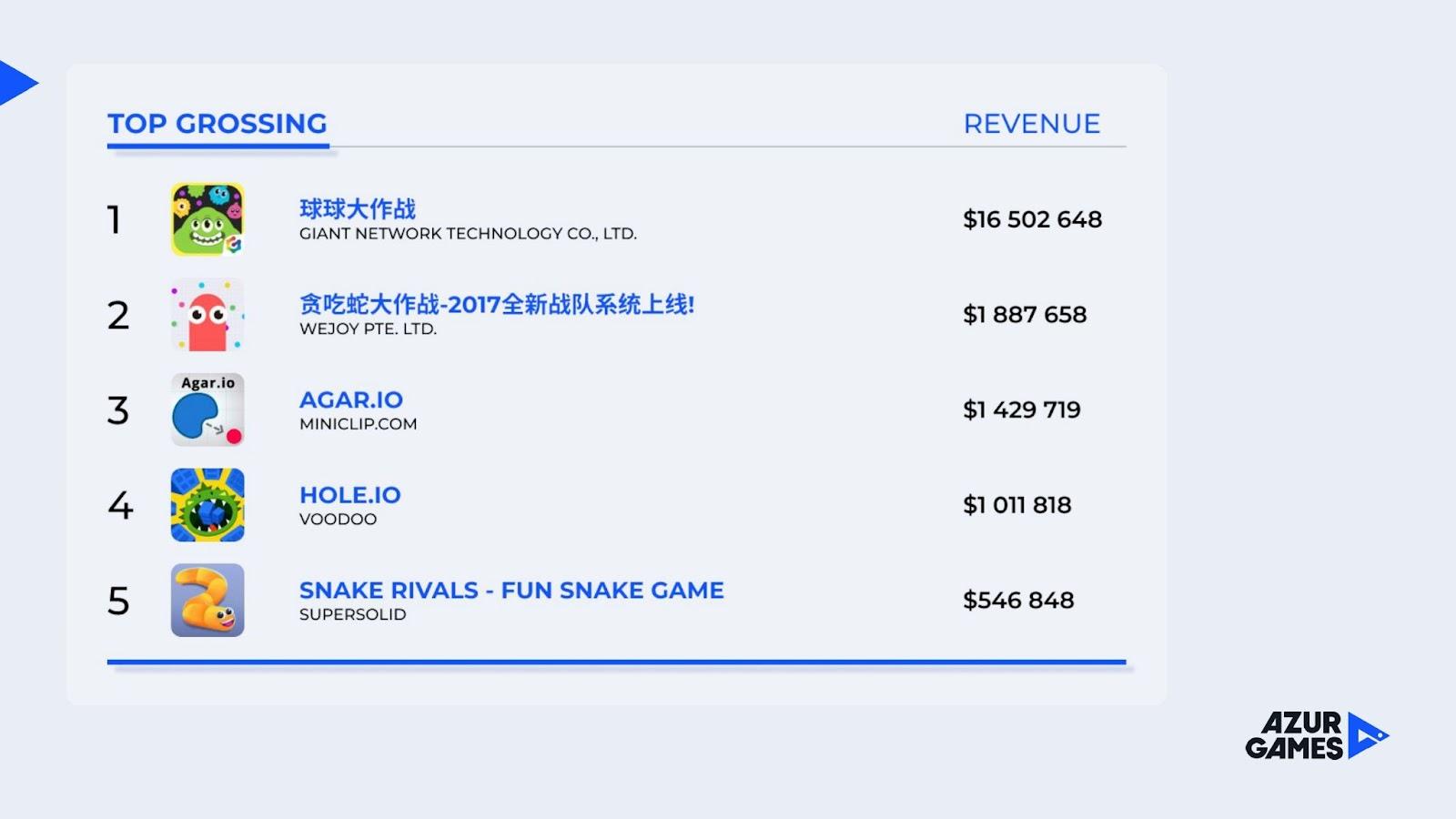

If we talk about decent indicators of in-game purchases in the .io genre, then it should be taken into account that here the first place in revenue is occupied by a game called Battle of Balls, very popular in Asia. It takes about 80% of all revenue among the top 5 games in this genre. Therefore, when working with any analytical tools, you need to be very careful.

How do developers behave against the background of downloads and revenue?

We are seeing more and more prototypes of puzzles, clickers, runners and strategies. But each subgenre has its own pace, so it’s always worth analyzing your competitors and decomposing their products. Only after that it makes sense to take risks, to do something trending.

Below are the first candidates for decomposition.

It is obvious that idlers and, for example, puzzles are now in trend.

However, in our opinion, it is now worth more “delving” into the market, constantly monitoring what is happening on it and analyzing it yourself. This is the only way to increase your chances of success. A blind race for trends is not a fact that it will give something.

In general, not the easiest times are coming for developers. Yes, we expect some niche growth, but more at the expense of low-income regions.

At the same time, the games themselves bring less and less profit today, so instead of looking for a hit, it’s better to focus on creating several projects with average metrics. This can be a good source of funds, a foundation that will allow you to focus on something deeper in the future.